What's the Best Way to Protect a House From Medicaid -- Gift or Trust?

My parents are getting older and they want to make sure their home is not taken from them if they should end up in a nursing...

Read more Elder Law Answers

Elder Law Answers

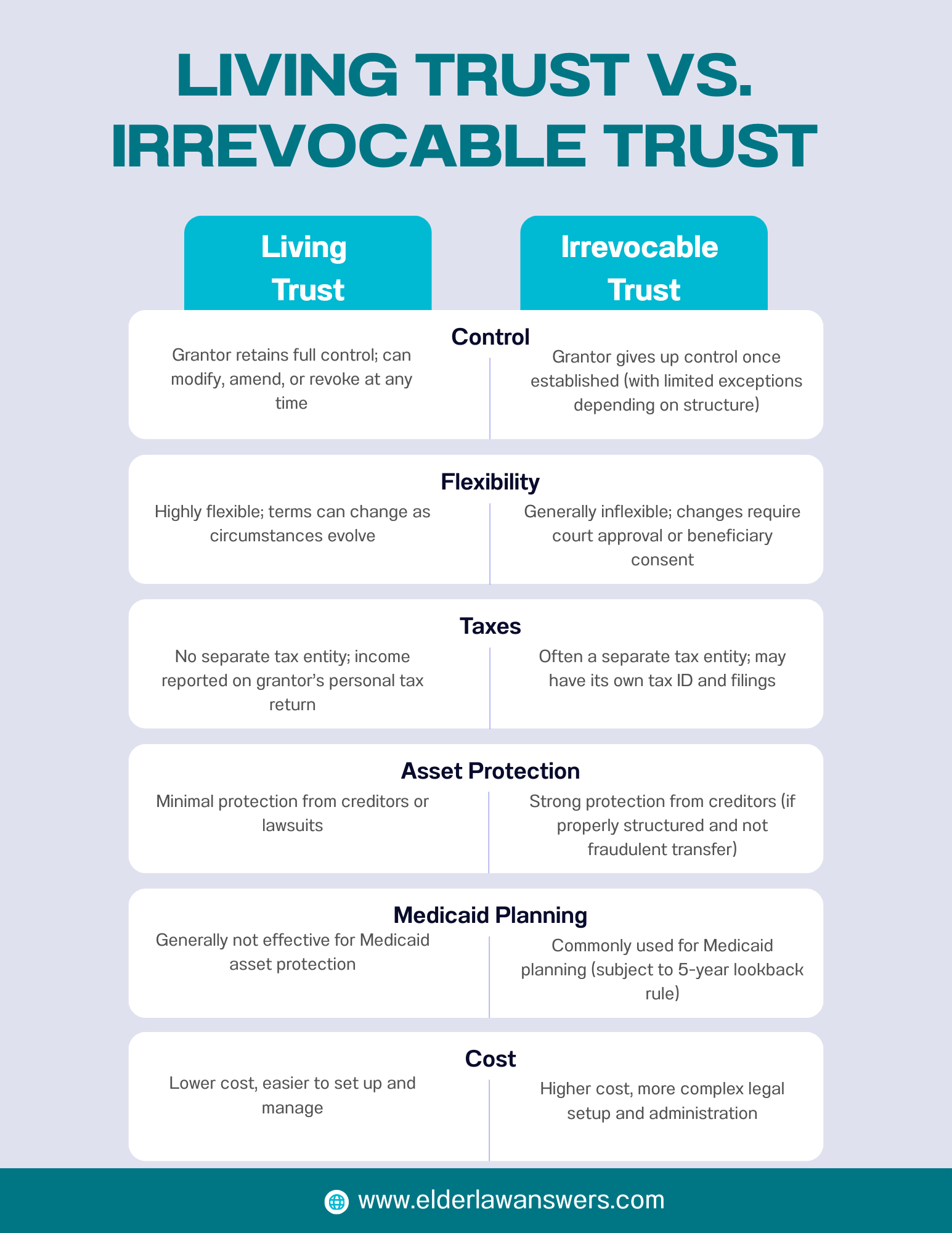

Trusts can be useful tools to protect your assets, save on estate taxes, or set aside money for a family member. You may be considering adding this kind of legal document to your own estate plan. Before you commit to establishing a trust, make sure you understand the differences between revocable (living) and irrevocable trusts. Each type of trust offers its own advantages and downsides, depending on their purpose.

Trusts can be useful tools to protect your assets, save on estate taxes, or set aside money for a family member. You may be considering adding this kind of legal document to your own estate plan. Before you commit to establishing a trust, make sure you understand the differences between revocable (living) and irrevocable trusts. Each type of trust offers its own advantages and downsides, depending on their purpose.

These two main types of trusts differ in structure and with regard to taxes. However, both serve as tools for setting aside your hard-earned assets and then passing them on according to your specific wishes. They can protect one’s property, safeguard a family’s financial future, and provide tax-saving strategies.

Once you establish an irrevocable trust, you cannot cancel or revoke it. The person creating the trust, sometimes called the “grantor,” transfers assets into the trust and permanently gives up all claims to them. A trustee then carries out the instructions spelled out in the trust. Any changes to the terms of the trust document require the consent of the trust’s beneficiaries.

In contrast, a revocable or living trust offers more flexibility. The grantor of a living trust still owns and controls the assets and can make changes at any time. A living trust also has a trustee. This individual would take over management of the trust if the owner is no longer capable of doing so.

Note that an institution can serve in the role of a trustee.

You may worry that you will not be able to make any adjustments to an irrevocable trust if your wishes change over time. In fact, it is possible to create a new trust with revised terms. You can then move the assets from the original trust into it.

Read more about this process of modifying an irrevocable trust, through decanting, in another article.

Both types of trusts offer tax advantages, although these differ in key ways.

As an irrevocable trust is considered a separate entity, it must have its own tax returns filed annually under its tax ID number. Irrevocable trusts can incur additional costs if a certified public accountant (CPA) is necessary for tax preparation.

Because it is a trust and not an individual, the irrevocable trust can’t qualify for the various deductions and exemptions that individuals can claim on their returns. Also, higher rates apply at lower income levels.

For example, an irrevocable trust is subject to the highest federal tax rate of 37 percent if its income exceeds $15,200 in 2024. (Note that this is a much lower ceiling than for individuals. The maximum tax rate for an individual would begin after $609,350 of ordinary income, as of 2024.)

Assets within a living trust, however, are still considered the property of the trust owner. Any income you earn from this type of trust is filed along with your other income.

Also, the assets of the trust belong to the owner’s estate. This means they are taxed accordingly upon the owner’s death. For this reason, wealthy families may choose to transfer a portion of their assets into an irrevocable trust. This can help in keeping the value of their estate below federal and state exemptions.

One key advantage of irrevocable trusts is that lawsuits and creditors cannot access their assets. A living trust offers no such protection because the trust assets are still part of the owner’s property.

Living trusts are an option for people who don't need all the layers of protection but still want to set up some provisions for the future. A living trust works well to set aside assets should the grantor ever become unable to manage their finances in the future, potentially because of illness or old age.

With this type of trust, the grantor controls the property while they are competent. The trustee can take over this function if the grantor loses this capacity.

You may be trying to navigate specific considerations, such as planning for estate taxes or protection from creditors. Perhaps you are looking to provide for the future well-being of a family member who has a disability. In certain cases, an irrevocable trust might be the better way to go. An experienced estate planner will have the best answers and estate planning tools to suit your particular circumstances.

Keep in mind that this is general advice only. An estate planner in your state versus another state may treat specific situations differently, as state laws vary. Contact a local estate planning attorney for advice on how to handle your situation using different types of trusts. Find a qualified attorney near you today for further guidance.

For additional reading, consider checking out the following articles: